This is an update to the original November 2025 report. Read the original here → The AI Factory: A 2024–2025 Overview

This is an executive brief synthesizing the key findings and action items from my full AI Infrastructure Supercycle 2026 report. Designed for decision-makers who need the “so what” without the footnotes. Download the full PDF below.

What Is This and Why Does It Matter?

The AI infrastructure buildout has stopped being a technology story. Between November 2025 and February 2026, it became an industrial, energy, and geopolitical one.

This brief maps five interconnected shifts — faster chip cycles, exploding capital spending, the switch to nuclear power, regulatory backlash, and Southeast Asia’s rise as a digital hub — and what each means for decisions you need to make now.

One-sentence summary: The race to build AI Superfactories has entered a phase where whoever secures firm power, future-proof infrastructure, and regulatory goodwill first will win — and the window to act is compressing fast.

The Six Most Important Points

A. The chip cycle just compressed from 2 years to 1

NVIDIA is now releasing a new GPU architecture every year — Blackwell → Blackwell Ultra → Rubin. Anyone who bought Blackwell hardware in late 2025 will find it eclipsed by Rubin in 6–9 months. The practical implication: you can no longer design a data center around a specific chip. Infrastructure must be built chip-agnostic — liquid cooling and power systems that can support whatever comes next.

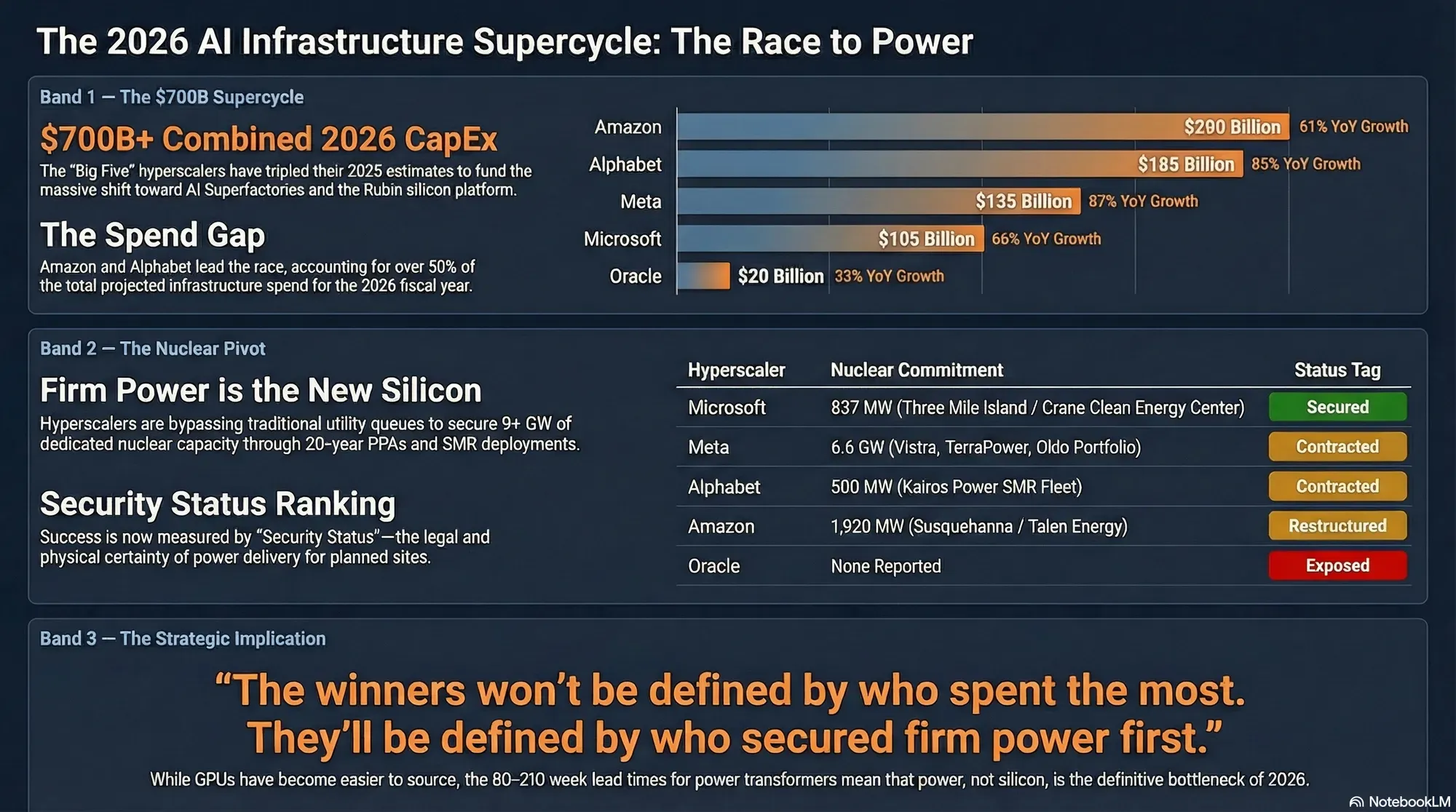

B. $700 billion is being spent by just five companies in 2026

Amazon, Google, Meta, Microsoft, and Oracle will collectively invest over $700 billion in AI infrastructure this year alone — nearly 3× the 2025 figure. They’re borrowing aggressively to do it, with a projected $1.5 trillion in debt issuance. The market is demanding proof that this spending converts into revenue, which means the pressure to monetize AI quickly is intense and growing.

The $700B supercycle, the nuclear pivot, and the strategic implication. Source: AI Infrastructure Supercycle 2026 Report.

The $700B supercycle, the nuclear pivot, and the strategic implication. Source: AI Infrastructure Supercycle 2026 Report.

C. Nuclear power is now the only credible energy strategy at scale

Grid connections and gas turbines are no longer sufficient or acceptable. Every major hyperscaler has signed long-term nuclear agreements: Microsoft’s $16B Three Mile Island deal, Google’s SMR fleet, Meta’s 6.6 GW portfolio, Amazon’s Susquehanna restructure. Nuclear is being chosen because it is the only firm (always-on) power source that is also carbon-free — the two non-negotiable requirements for multi-gigawatt AI facilities.

D. Building without permits is now a company-threatening risk

xAI’s approach — install turbines first, apply for permits later — has triggered NAACP lawsuits, state regulatory hearings, and federal scrutiny. The risk isn’t just fines; it’s injunctions that shut down operations and an “environmental bad actor” label that drives away ESG capital. This is now a standard planning assumption: skip the permits and you may lose the facility entirely.

E. Thailand is the place to be in Southeast Asia — but it has real constraints

Thailand’s data center pipeline (2.87 GW) is 3.7× that of Indonesia. AWS, Google, and ByteDance have all committed. The government offers 8-year tax holidays and fast-track licensing. But the country faces a cooling energy penalty (40% of power vs. 30% globally), serious water scarcity risk by 2030, a skilled labor shortage in technical roles, and Bangkok grid caps that force projects to relocate to Chonburi and Rayong.

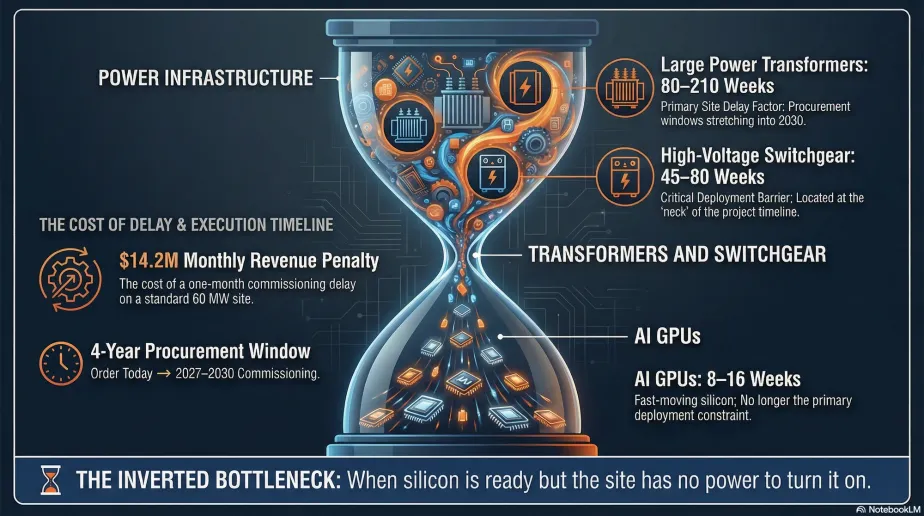

F. The real bottleneck is no longer GPUs — it’s power transformers

GPU lead times have dropped to 8–16 weeks. But large power transformers now take 80–210 weeks (up to 4 years) to deliver, and high-voltage switchgear runs 45–80 weeks. A single month’s delay in commissioning a 60 MW facility costs roughly $14.2 million in lost revenue. Whoever locks in electrical infrastructure contracts first wins.

Risks to Watch

🔴 High — Act Now

Transformer & switchgear lead times: With 80–210 week delivery windows, any data center project not already in the procurement queue for high-voltage equipment is effectively 2–4 years behind schedule. This is the single biggest risk to deployment timelines in 2026.

Nuclear supply deficit: Even with unprecedented demand, uranium supply and reactor component manufacturing are lagging. A structural power deficit is expected in late 2026, which could strand or delay new AI facilities counting on nuclear supply coming online.

Obsolescence trap: Enterprises that locked in large Blackwell deployments in late 2025 face rapid depreciation. Hardware designed for a 3–5 year amortization cycle is being eclipsed in under 12 months. On-premises deployments are particularly exposed.

🟡 Medium — Monitor Closely

Regulatory tightening: New federal executive orders and state-level legislation in California and Virginia are targeting data center power draw and community impact. The permitting environment is tightening industry-wide.

Thailand water stress: By 2030, an estimated 40% of Asia Pacific data centers will face high or extreme water stress. Facilities relying on evaporative cooling need water resilience plans now, before construction.

Debt sustainability: Hyperscalers are taking on $1.5 trillion in projected debt. If AI revenue conversion is slower than expected, the risk of CapEx pullback rises sharply.

Bangkok grid cap: MEA currently caps new connections above 30 MW in metropolitan Bangkok unless the developer self-funds grid upgrades, adding 18–24 months to timelines.

🟢 Lower — Stay Informed

NVIDIA market share: Custom ASICs (Google TPU, AWS Trainium2) are growing at 22% per year in the inference market. NVIDIA’s near-monopoly is intact for training but may erode in inference over 3–5 years.

Thailand talent gap: Over 50% of Southeast Asian data center operators struggle to fill critical technical roles, adding 6–12 months to project timelines as a recurring assumption.

ESG capital flight: Institutional investors are increasingly treating environmental compliance as a precondition for investment. Facilities in regions with poor air quality records may face higher cost of capital or exclusion from certain funds.

Key Timelines

| Timeframe | What Happens |

|---|---|

| Now → Q2 2026 | Rubin architecture enters volume production. Infrastructure not designed for next-gen cooling will be obsolete at delivery. |

| H2 2026 | NVIDIA Rubin ships. Blackwell hardware begins rapid depreciation in enterprise deployments. |

| 2028 | Microsoft’s Three Mile Island nuclear restart comes online. First major hyperscaler nuclear supply activated. |

| 2030 | Google’s first Kairos SMR targeted for deployment. ~40% of Asia Pacific data centers projected to face high water stress. |

| 2030–2035 | Meta’s 6.6 GW nuclear portfolio comes fully online. Inference workloads overtake training as dominant compute requirement. |

| Ongoing (80–210 wk lead) | Large power transformer orders placed today won’t arrive until 2027–2030. The procurement window for on-time projects is already closing. |

10 Actions to Take Now

🔴 Immediate — Act Within Days to Weeks

| # | Action |

|---|---|

| 1 | Audit transformer & switchgear procurement for any existing or planned data center investments. With 80–210 week lead times, orders placed today won’t arrive until 2027–2030. If you’re not in queue, you’re already behind. |

| 2 | Re-underwrite Blackwell ROI. With Rubin arriving H2 2026 and delivering 2.5× better inference performance, any on-premises GPU deployment made in 2025 needs a revised amortization model against a 12-month obsolescence window — not 3–5 years. |

🟡 Near-Term — Act Within 1–3 Months

| # | Action |

|---|---|

| 3 | Prioritize Thailand over Indonesia for Southeast Asia data center development — but site in Chonburi, Rayong, or the EEC, not Bangkok. The MEA’s 30 MW grid cap adds 18–24 months to any Bangkok project without self-funded grid upgrades. |

| 4 | Require chip-agnostic infrastructure design. Any new data center must support rack densities from 80 kW through 140 kW without full redesign. Building around a specific chip generation is no longer viable. |

| 5 | Make PPA status a gating criterion. No committed firm power (nuclear, geothermal, or front-of-meter utility) = no investment. Projects without secured baseload carry outsized delivery and cost risk. |

| 6 | Commission a water resilience assessment for any Thailand or Asia Pacific site under consideration. By 2030, 40% of regional data centers will face high or extreme water stress. This needs to be in the design brief, not the post-mortem. |

🟢 Strategic — Act Within 3–12 Months

| # | Action |

|---|---|

| 7 | Review NVIDIA concentration risk in inference. Custom ASICs (Google TPU, AWS Trainium2) are growing at 22% vs. 19% for GPUs in the inference segment. Current allocations may not reflect the inference-first shift underway. |

| 8 | Apply the Memphis test to every infrastructure thesis. The xAI precedent means unpermitted or community-opposed sites are now a standard exclusion criterion for institutional ESG capital. If it wouldn’t survive a NAACP challenge, it’s a liability. |

| 9 | Track the nuclear supply chain as a leading indicator. Uranium availability and reactor component manufacturing are lagging demand. A structural power deficit in late 2026 hits unlocked capacity first — watch this as an early warning system. |

| 10 | Monitor Thailand’s UGT program. The proposed 37% reduction in the UGT1 premium signals the government’s intent to stay competitive with Malaysia and Indonesia on green energy costs — directly relevant for ESG-reporting tenants evaluating the region. |

Download the Full Report

The full 13-page report includes detailed technical specifications, hyperscaler CapEx matrices, supply chain lead time analysis, Thailand market data, and complete works cited.

📄 Download the Full Report (PDF)

This is part of an ongoing quarterly series tracking the AI infrastructure buildout. The original November 2025 report is also available. To receive future updates, connect with me on LinkedIn.

About the Author

Carlos Granier is a Tech Founder, CTO, and AI Strategist with 25 years of experience building at the intersection of technology and business. He co-founded Pongalo, one of the first US Hispanic OTT platforms, and built a YouTube MCN to 200M+ monthly views. He now helps founders and executives implement AI as practical infrastructure. Based in Miami, Florida.

Let's Connect

If you want to hire me or get in touch about something or just to say hi, reach out on social media or send me an email.

- X (Twitter) /

- Threads /

- Instagram /

- GitHub /

- LinkedIn / 📧